Smart manufacturing investments. Source: GP Bullhound

Continuing improvements in software and hardware are leading to trends such as Manufacturing-as-a-Service, hyper-personalization of products on demand, and a reinvention of the capital goods economy, found a new study. Last month, GP Bullhound issued a new report titled “Smart Manufacturing: The Rise of the Machines.”

The report provided a global, in-depth look at how smart manufacturing gained momentum between 2013 and 2018. It also drew conclusions about the potential future for manufacturing in terms of growth, investment, and the value of data. With robotics still largely serving manufacturing, engineers can get a glimpse of trends for which to prepare.

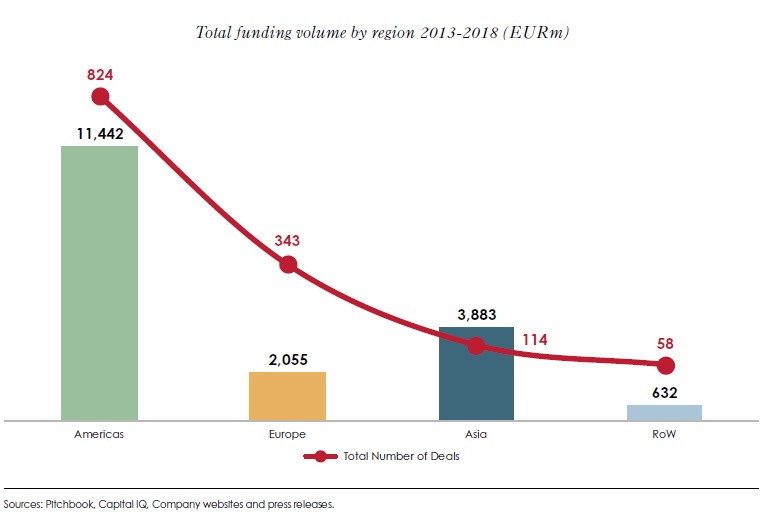

GP Bullhound reviewed the value of smart manufacturing transactions. China and Japan have led in smart manufacturing, with a market value of $28 billion, according to the technology advisory and investment firm. Europe followed with $24 billion, and the U.S. lagged at $20 billion.

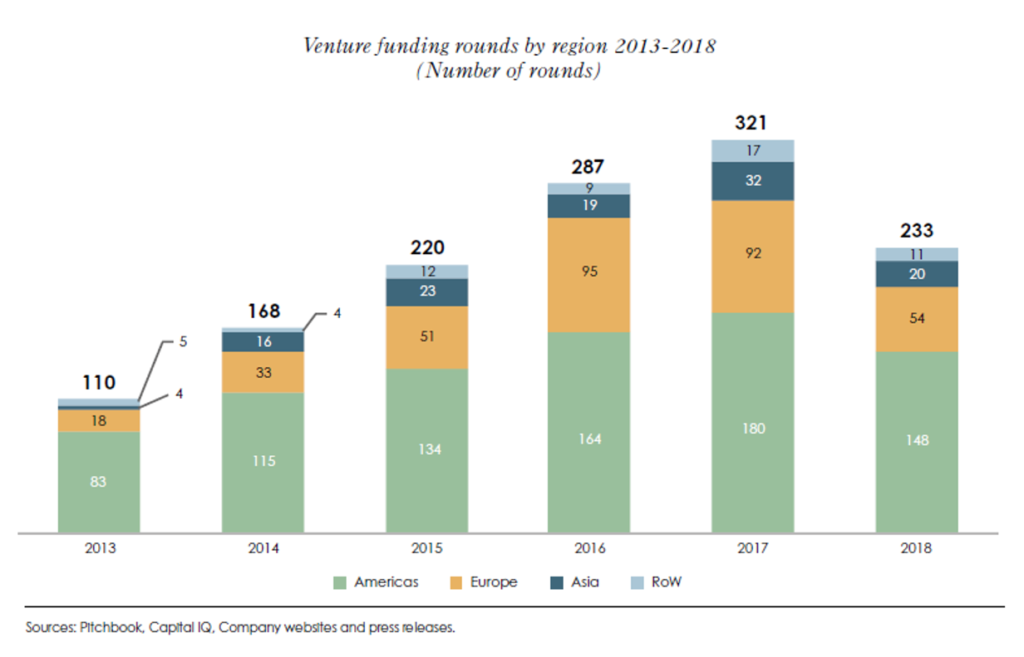

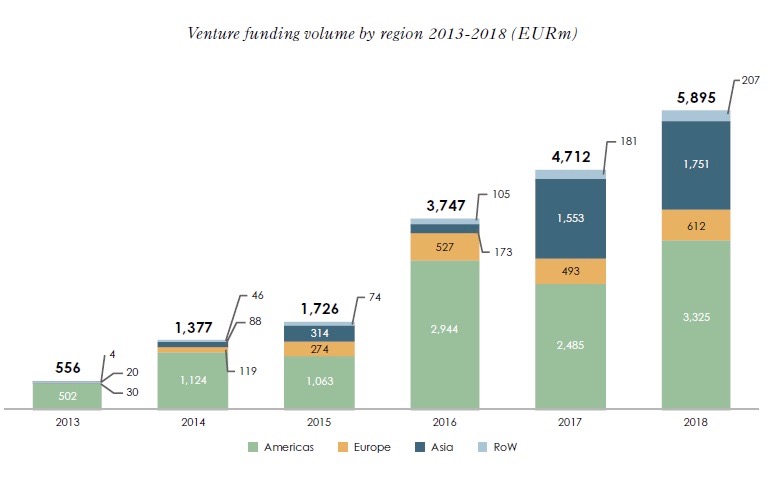

The report found 1,300 venture capital transactions worldwide, worth a total of $17.4 billion. The U.S. led in investments, with American startups receiving $11.4 billion, compared with $3.9 billion in Asia and $2.1 billion in Europe. GP Bullhound also found $37.7 billion in mergers and acquisitions during the five-year period.

Sources: Pitchbook, Capital IQ, company websites, press releases, GP Bullhound

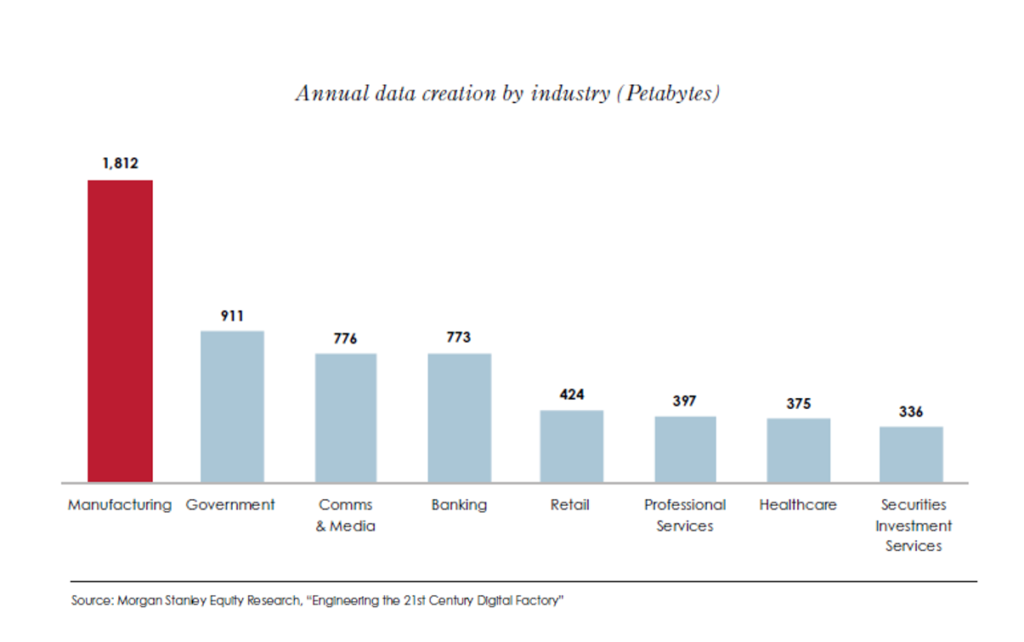

In addition, the report noted that data is growing in value, despite debates over how and whether production should be automated.

Dr. Nikolas Westphal, director at GP Bullhound, answered several questions from The Robot Report about the study’s findings:

Whether we call it “smart manufacturing,” “Industry 4.0,” or something else, the combination of machine learning, big data, the Internet of Things (IoT), and robotics is arriving, according to your report. But how ready are most companies — especially those outside the electronics and automotive verticals — for it?

Westphal: Smart manufacturing readiness is something that we discussed with several of our interview partners, including interviewees from leading European software houses and IoT platforms.

The current state seems to be that most OEMs are substantially increasing the density of IoT devices within their equipment in order to make it “smart” and are also working on the required digital platforms. As “smart” equipment proliferates, more and more manufacturing operators of all sizes will start to increasingly use methodologies of smart manufacturing.

Source: GP Bullhound

When it comes to digitization by industry, our research indeed indicates that electronics and automotive are furthest down the line on the journey to end-to-end digitization. In general, I would say that today, industries with the highest scale effects are also the most automated. With the emergence of smaller, more flexible robotic equipment — such as collaborative robots, additive manufacturing, and data-driven factory design — we believe that also smaller players will be able to reap the rewards of smart automation.

Some of the companies featured in our report actually address this challenge for companies of all sizes. One example for this is Oden Technologies, which is featured in Section 2 of our report.

Investments in robotics and startups have slowed in the past quarter, but do you think that’s temporary and why?

Westphal: Quarterly VC funding data is notoriously hard to interpret, as it follows transaction cycles. Applying our search criteria for smart manufacturing startups, global VC funding in smart manufacturing in Q1 2019 has stood at €1.02 billion ($1.14 billion U.S.) across 73 deals versus €1.07 billion ($1.2 billion U.S.) in Q4 2018 [Source: Pitchbook]. As there is somewhat of a reporting lag, I expect the Q1 2019 figure to be gradually adjusted upward throughout the year.

Source: GP Bullhound

How might a cyclical economic recession affect spending on industrial automation and smart manufacturing?

Westphal: I believe that a recession may not necessarily long-term impact investments into industrial automation specifically. While replacement cycles may somewhat slow, efficiency will be increasingly important in a recession situation.

The section on productivity gains from smart manufacturing cites Volvo as an example. How is Volvo’s use of robots part of a technology cluster?

Westphal: The tables and the case studies were supplied by our feature partner Accenture. On the left-hand side of both Figure 1 and 2, you can see the different relevant technologies, on the right-hand side different industry verticals. The percentages indicate the incremental cost savings per employee in Figure 1 as well as the projected implied additional gains in market capitalization in Figure 2.

For example, in automotive, autonomous robots and AI seem to have the biggest impact, in addition to 3D printing, blockchain, and big data. Overall, Accenture believes that the combinatory effect of these technologies will add up to incremental cost savings per employee of 13.9% for automotive.

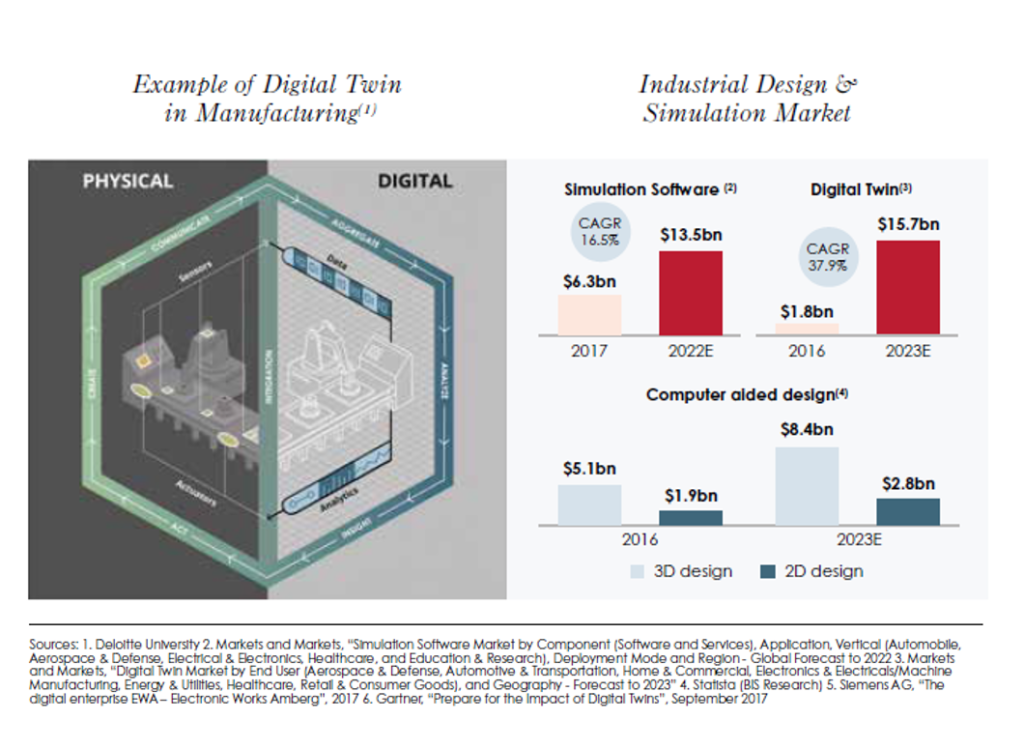

How much is simulation software being applied to the design and implementation of robotics? How far are we from “lights-out” manufacturing?

Westphal: This question is addressed to some extent by the feature of Brian Mathews of Bright Machines. Once the computer vision and control challenges have been addressed, lights out manufacturing should become a reality.

Source: GP Bullhound

Several robotics vendors have told us that they want to “keep humans in the loop,” so what sorts of processes are better for collaboration vs. full autonomy with “software-defined” manufacturing?

Westphal: From our interviews on the topic, it seems to me that high-volume, repetitive, but complex processes that require a high degree of accuracy are well-suited for full autonomy, while processes that require a high degree of versatility are better suited for collaboration.

In noteworthy mergers and acquisitions, why was Teradyne’s acquisition of Universal Robots included but not the creation of OnRobot or Honeywell‘s purchase of Intelligrated. Was there a reason for the omissions?

Westphal: The Teradyne-Universal Robots deal is featured on p. 33. Honeywell/Intelligrated is part of our database but not featured in the selected landmark transactions. We have not only selected those by size, but also other criteria like sector fit and visibility.

The creation of OnRobot is not shown in Section 3 as we weren’t able to find publicly available data on funding amount. OnRobot itself is featured as a notable company on p. 63 of the report.

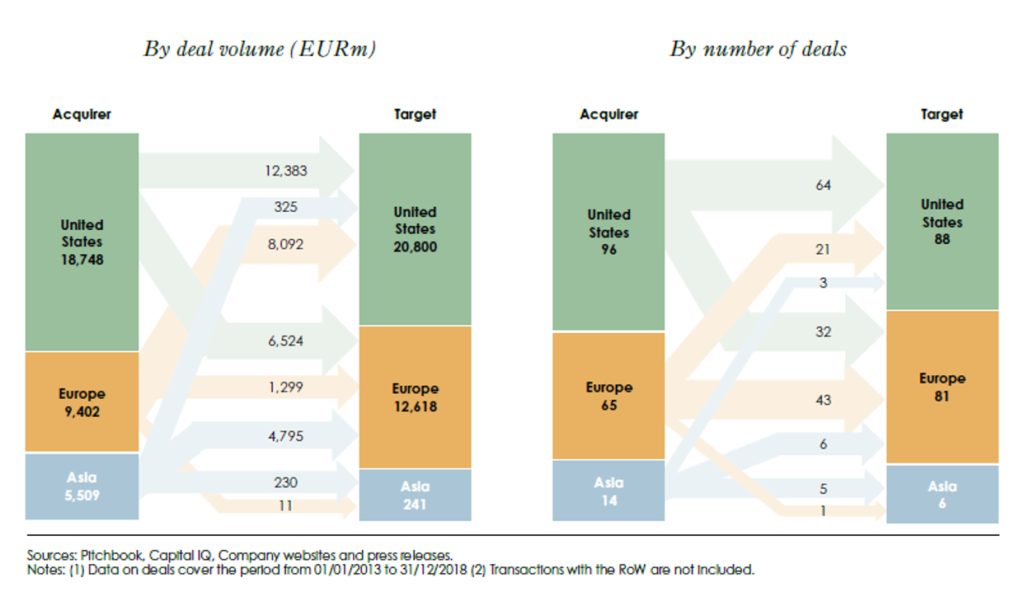

Will trade tensions between the West and China slow the trend to cross-border consolidation?

Westphal: It seems that Chinese outbound investment is really geared towards utilizing technologies in China’s huge manufacturing sector. Especially as Europe does not seem to engage in restrictive trade policies with China (yet), I would expect this trend to continue.

Cross-border deals. Source: GP Bullhound

Since GP Bullhound is watching investments in hardware and the software stack around smart manufacturing, has it identified any strategic leaders?

Westphal: We don’t provide investment advice. A selection of companies that we find interesting can be found on p. 62 and 63 of the report.

The post Smart manufacturing trends analyzed in GP Bullhound report appeared first on The Robot Report.

阅读原文